Identifying Your Business Risk Liabilities

Construction is a high-risk business, from the types of work being done to the financial uncertainty of payments and potential for lawsuits.

Insurers and surety companies view risk in terms of exposure to possible losses. Some losses have a higher probability of occurring than others and some will have greater consequences for your business.

What are the Risk Categories to Consider?

When identifying and analyzing risk, it’s helpful to see how risks fit into categories. Here are some

you should consider as you identify your own project risks. Use this checklist to look at your

construction business through a risk liability lens.

- Technical risks — poor design, insufficient site investigation, inadequate specifications and unavailability of materials

- Logistical risks — lack of equipment, spare parts, fuel, labor or transportation

- Construction risks — uncertainty of supplies, work site injuries and accidents, negligence, construction defects, and weather and seasonal uncertainty

- Contractual risks — legal and regulatory issues, and contract and labor disputes

- Financial risks — rising costs, payment delays, rising interest rates, lack of sales and unmanaged growth

- Project risks — improper management, inadequate allocation of resources, and unrealistic schedules or schedule changes

- Political risks — zoning disputes, lack of funding for public projects and political unrest

- Competitive risks — pressure to underbid a competitor, lack of profitability and being overextended

- Ethical risks — pressure to engage in political games or win bids using questionable tactics (This can put current and future contract engagements at risk.)

Categories and Subcategories of Risk

Now that you’ve made notes on the categories of risk for your construction business, take the next step.

Write down your risk areas and organize them. This checklist will help you identify specific liabilities.

- Write a description of each risk.

- What’s the likelihood that the risk will occur (low, medium, high)?

- What’s the potential impact on your business (low, medium, high)?

- How would the risk affect your workers or subcontractors?

- How would it affect scheduling?

- How would it affect the quality of materials?

- What about the safety of the job site?

- What actions can you take to mitigate the risk (options to correct or transfer the risk elsewhere)?

- What are the early warning signs of liability (several recurring accidents, invoices rarely go out on time, contracts are incorrect)?

- What methods will you use to communicate the risk, once recognized?

- Who owns the risk category and what methods will they use to handle risks previously reported to the owner?

- Do you have contingency plans or written guides?

- How will you communicate the steps of the written plan (formal training)?

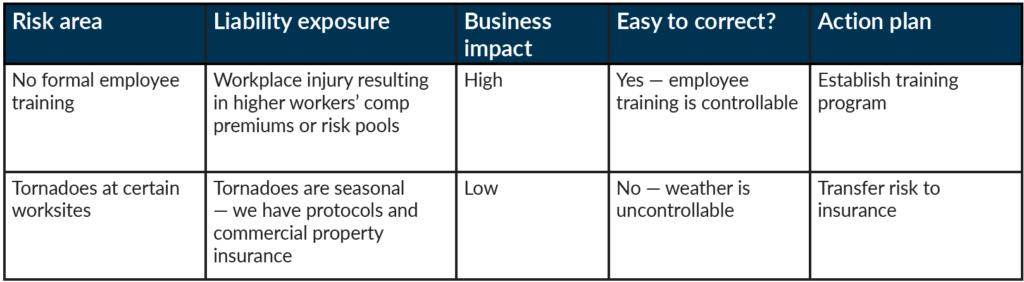

Consider how critical each of these areas is to the success of the job. You may find it helpful to create a table that lists each project area and its relative importance (low, medium, high).

Once you’ve figured out the risks, liabilities and potential business impact, assemble your risk management team. Your team will figure out the details of your risk management plan.

Use a risk management team checklist to help you and your team develop your plan.

To download the insight, click here